Plumbers Insurance

Plumber Insurance is essential for those in the sector. With so many things that can go wrong, relating to damage or injury, careful consideration is highly recommended. Some policies are also legally required for those with a workforce, no matter how small.

What You Need to Know About Plumbers Insurance

Plumbers Insurance is not an easy thing to define. The type of insurance required will often depend on the specifics of the business seeking a policy. This may include, for example, its size (turnover etc), how many employees need coverage and which extras will are relevant (such as tools and vehicle insurance). There are, however, some insurance policies that are vital, and even mandatory for plumbers, although not all policies are created equal.

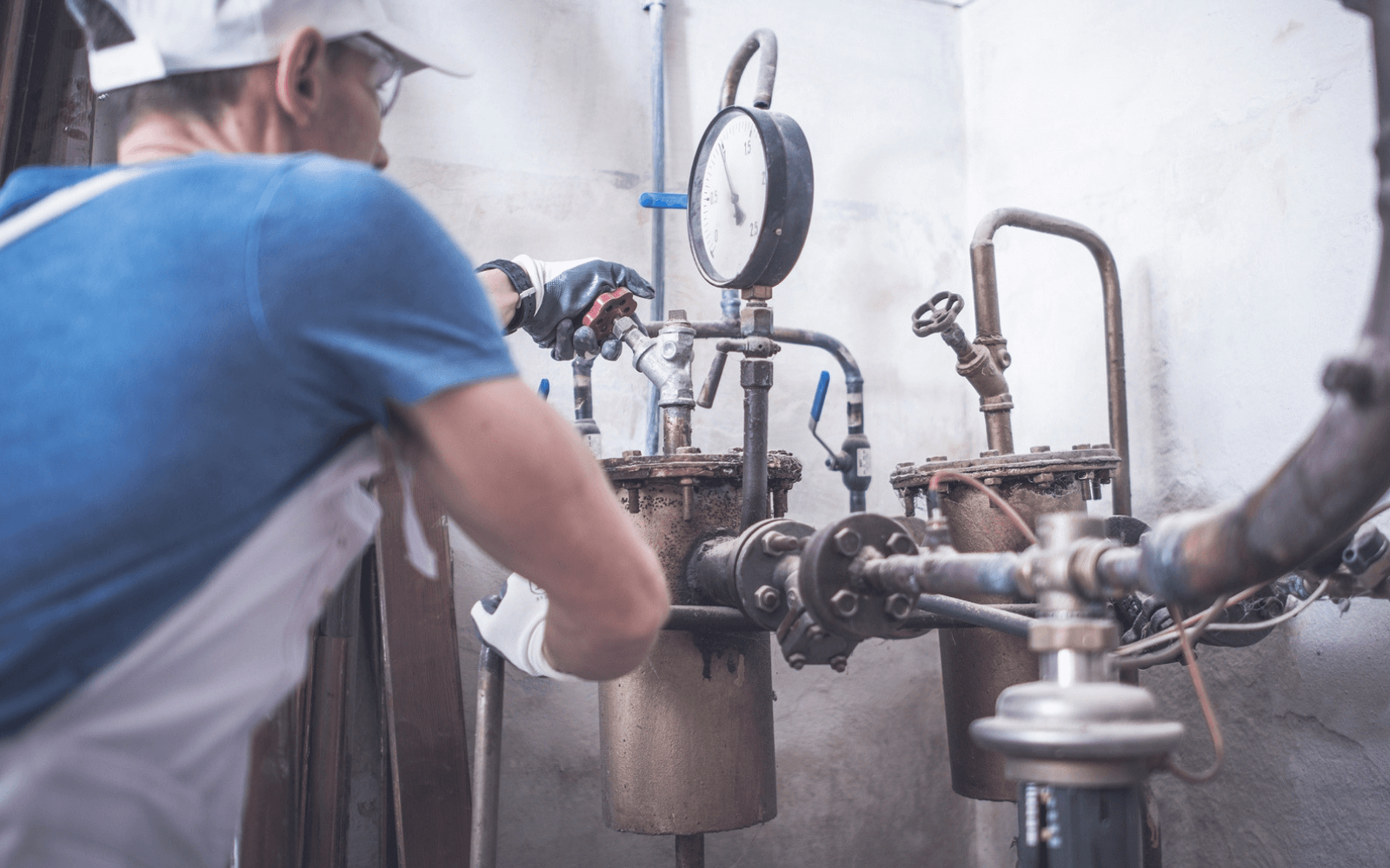

Another issue for businesses within the plumbing sector is the possibility for injury to both employers and employees (including any subcontractors). For plumbers, the risk is often heightened when the work undertaken happens on building sites or already damaged property. Such complications are not exclusive to the sector, but there are risks that are magnified particularly within certain situations. What’s more, any insurance incident can lead to work slowing down or stopping altogether. This can be disastrous for large projects if an uninsured business is liable.

Other Notable Features of Plumber Insurance

As previously touched upon, Plumber Insurance has many different aspects to it, some of which are legally mandatory. Understanding which are also important is paramount. The main policy features typically include:

Public Liability Insurance

Public Liability is not legally mandatory, but it is one of the most important insurance policies a business in the plumbing sector can undertake. Also referred to as PL Insurance, the policy covers businesses for claims against them relating to illness, injury and third party property damage. It should also be noted that some large commercial projects will contractually oblige a business to seek out Public Liability Insurance.

Employers’ Liability Insurance

Any employees a plumber hires, whether it be an apprentice, part time employee or full time worker, means they have to take out employer Insurance. In fact, a minimum coverage of £5m is legally required for all businesses with a workforce in the sector, although most Employer Liability policies cover up to £10m as standard in practice as a matter of course. The policy should cover illness and injury suffered by an employee that the business is liable for, as well as any damage to their property.

Tools & Equipment Cover

Some tools and equipment used for plumbing can be of extremely high value. As such, insuring tools and equipment is vital, particularly if a business cannot function without them. While this policy is considered by some to little more than an extra, the loss of such equipment can be terminal. It should be noted that a clause to ensure all equipment is secured is standard for such policies and failure to do so can lead to the insurance policy being annulled.

Buildings Cover

Depending on the insurance company, Buildings Insurance is sometimes available to add to other policies for plumbing businesses. Often these “Add-ons” are relatively cheap if larger policies are sought, such as an over-arching business style of policy. Buildings insurance is worthwhile if a plumber has a premises that is integral to the business and may even include contents coverage.